Downloads

Umsatz

Beschreibung

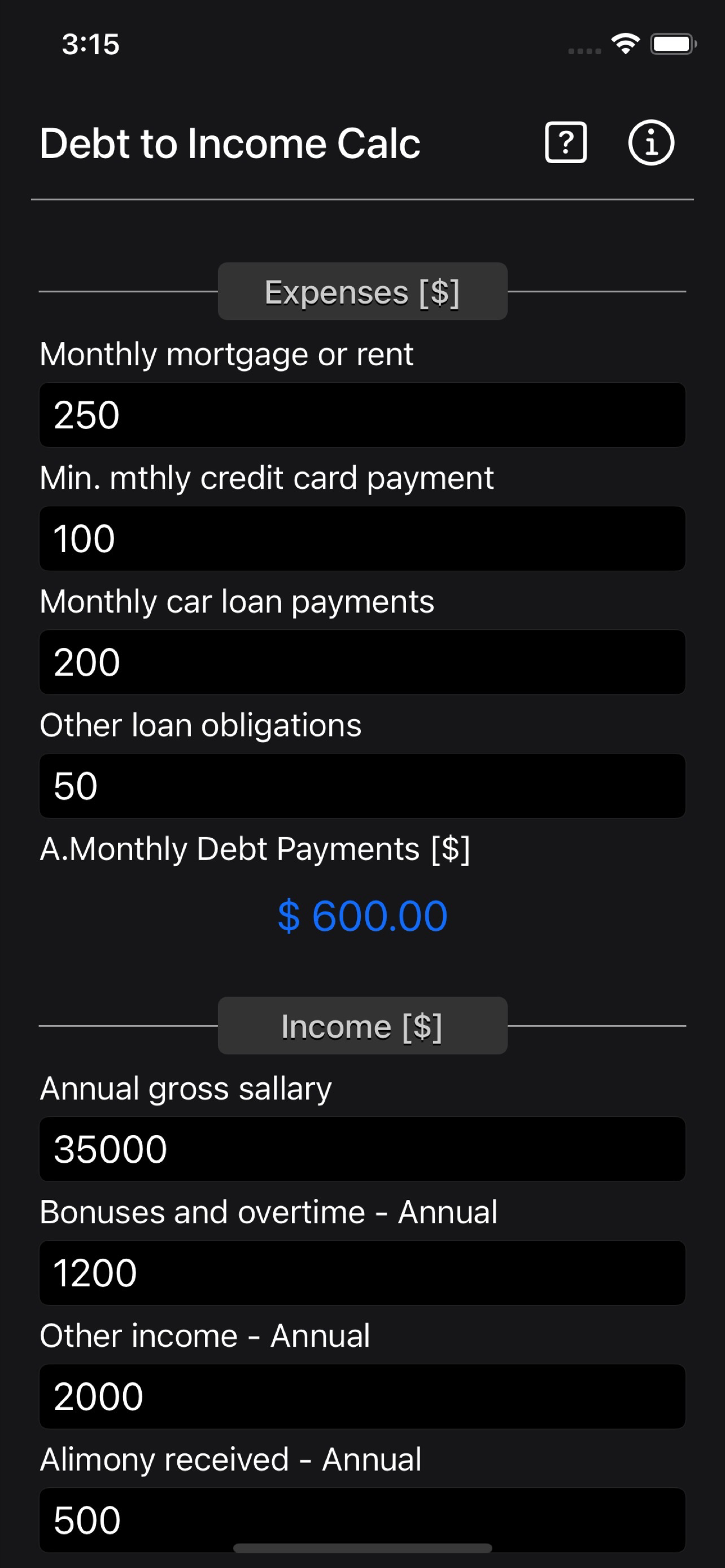

Debt 2 Income Calculator, This debt to income ratio app has been created to help you calculate how much debt you can afford. Use this app to determine the ratio between your current income and current debt.

You can use this debt-to-income ratio calculator, also referred to as a DTI calculator, to figure out if you might be at risk of carrying too much debt or if you qualify for a loan of a given size. In general, lenders apply certain rules when evaluating someone that has applied for credit. The calculator performs both front-end, as well as back-end debt-to-income calculations.

Debt-to-income ratio

Percentage of monthly income that is spent on debt payments, including mortgages, student loans, auto loans, minimum credit card payments and child support.

Debt payments / income

For example: Peter earn $10,000 a month. His total debt payments are $3,800 a month. His debt-to-income ratio is 38 percent.

$3,800 / $10,000 = 0.38

Front-end ratio

A standard rule for lenders is that your monthly housing payment (principal, interest, taxes and insurance) should not take up more than 28 percent of your income before taxes. This debt-to-income ratio is called the "housing ratio" or "front-end ratio."

Back-end ratio

Lenders also calculate the "back-end ratio." It includes all debt commitments, including car loan, student loan and minimum credit card payments, together with your house payment. Lenders prefer a back-end ratio of 36 percent or less.

Ratios aren't carved in stone

Those recommended ratios (28 percent front-end and 36 percent back-end) aren't ironclad. In many cases, lenders approve applicants with higher debt-to-income ratios. Under the "qualified mortgage rule," federal regulations give legal protection to well-documented mortgages with back-end ratios (all debts, including house payments) up to 43 percent.

"That's been one of the bigger drivers (of affordability) because that is basically drawing a box around what's a qualified mortgage," says Tim Skinner, home lending sales and service manager for Huntington Bank in Columbus, Ohio. "A large portion of the lending community has decided to stay in that box."

Credit history:

If you have a good credit history, you are likely to get a lower interest rate, which means you could take on a bigger loan. The best rates tend to go to borrowers with credit scores of 740 or higher.

Thanks for your support and do visit nitrio.com for more apps for your iOS devices.

Ausblenden

Mehr anzeigen...

You can use this debt-to-income ratio calculator, also referred to as a DTI calculator, to figure out if you might be at risk of carrying too much debt or if you qualify for a loan of a given size. In general, lenders apply certain rules when evaluating someone that has applied for credit. The calculator performs both front-end, as well as back-end debt-to-income calculations.

Debt-to-income ratio

Percentage of monthly income that is spent on debt payments, including mortgages, student loans, auto loans, minimum credit card payments and child support.

Debt payments / income

For example: Peter earn $10,000 a month. His total debt payments are $3,800 a month. His debt-to-income ratio is 38 percent.

$3,800 / $10,000 = 0.38

Front-end ratio

A standard rule for lenders is that your monthly housing payment (principal, interest, taxes and insurance) should not take up more than 28 percent of your income before taxes. This debt-to-income ratio is called the "housing ratio" or "front-end ratio."

Back-end ratio

Lenders also calculate the "back-end ratio." It includes all debt commitments, including car loan, student loan and minimum credit card payments, together with your house payment. Lenders prefer a back-end ratio of 36 percent or less.

Ratios aren't carved in stone

Those recommended ratios (28 percent front-end and 36 percent back-end) aren't ironclad. In many cases, lenders approve applicants with higher debt-to-income ratios. Under the "qualified mortgage rule," federal regulations give legal protection to well-documented mortgages with back-end ratios (all debts, including house payments) up to 43 percent.

"That's been one of the bigger drivers (of affordability) because that is basically drawing a box around what's a qualified mortgage," says Tim Skinner, home lending sales and service manager for Huntington Bank in Columbus, Ohio. "A large portion of the lending community has decided to stay in that box."

Credit history:

If you have a good credit history, you are likely to get a lower interest rate, which means you could take on a bigger loan. The best rates tend to go to borrowers with credit scores of 740 or higher.

Thanks for your support and do visit nitrio.com for more apps for your iOS devices.

Screenshots

Debt 2 Income Calculator Häufige Fragen

-

Ist Debt 2 Income Calculator kostenlos?

Ja, Debt 2 Income Calculator ist komplett kostenlos und enthält keine In-App-Käufe oder Abonnements.

-

Ist Debt 2 Income Calculator seriös?

Nicht genügend Bewertungen, um eine zuverlässige Einschätzung vorzunehmen. Die App benötigt mehr Nutzerfeedback.

Danke für die Stimme -

Wie viel kostet Debt 2 Income Calculator?

Debt 2 Income Calculator ist kostenlos.

-

Wie hoch ist der Umsatz von Debt 2 Income Calculator?

Um geschätzte Einnahmen der Debt 2 Income Calculator-App und weitere AppStore-Einblicke zu erhalten, können Sie sich bei der AppTail Mobile Analytics Platform anmelden.

Benutzerbewertung

Die App ist in Japan noch nicht bewertet.

Bewertungsverlauf

Debt 2 Income Calculator Bewertungen

Keine Bewertungen in Japan

Die App hat noch keine Bewertungen in Japan.

Store-Rankings

Ranking-Verlauf

App-Ranking-Verlauf noch nicht verfügbar

Kategorien-Rankings

|

Diagramm

|

Kategorie

|

Rang

|

|---|---|---|

|

Top Bezahlt

|

|

426

|

Debt 2 Income Calculator Konkurrenten

Debt 2 Income Calculator Installationen

Letzte 30 Tage

Debt 2 Income Calculator Umsatz

Letzte 30 TageDebt 2 Income Calculator Einnahmen und Downloads

Gewinnen Sie wertvolle Einblicke in die Leistung von Debt 2 Income Calculator mit unserer Analytik.

Melden Sie sich jetzt an, um Zugriff auf Downloads, Einnahmen und mehr zu erhalten.

Melden Sie sich jetzt an, um Zugriff auf Downloads, Einnahmen und mehr zu erhalten.

App-Informationen

- Kategorie

- Finance

- Herausgeber

- Heng Jia Liang

- Sprachen

- English

- Letzte Veröffentlichung

- 1.0 (vor 1 Jahr )

- Veröffentlicht am

- Mar 14, 2023 (vor 1 Jahr )

- Auch verfügbar in

- Vereinigte Staaten, Pakistan, Italien, Japan, Südkorea, Kuwait, Kasachstan, Libanon, Mexiko, Malaysia, Nigeria, Niederlande, Norwegen, Neuseeland, Peru, Philippinen, Indien, Polen, Portugal, Rumänien, Russland, Saudi-Arabien, Schweden, Singapur, Thailand, Türkei, Taiwan, Ukraine, Vietnam, Südafrika, Dominikanische Republik, Argentinien, Österreich, Australien, Aserbaidschan, Belgien, Brasilien, Belarus, Kanada, Schweiz, Chile, China, Kolumbien, Tschechien, Dänemark, Vereinigte Arabische Emirate, Algerien, Ecuador, Ägypten, Spanien, Finnland, Frankreich, Vereinigtes Königreich, Griechenland, Sonderverwaltungsregion Hongkong, Ungarn, Indonesien, Irland, Israel

- Zuletzt aktualisiert

- vor 5 Tagen

- © 2024 AppTail.

- Unterstützung

- Privacy

- Terms

- All Apps